Will Gas and Oil Price Continue to Decline September 2017

Winter Fuels Outlook, October 2022

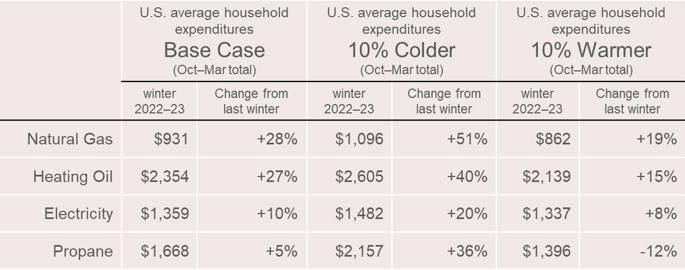

Many households across the United States are likely to spend more on energy in the winter of 2022–23 compared with recent winters. Higher forecast energy expenditures are the result of higher fuel prices, combined with higher heating demand because of a forecast of slightly colder weather than last winter.

Forecast expenditures also vary significantly across U.S. regions and fuels for this winter (Winter Fuels Outlook table). The price and expenditure values presented in this report are in nominal terms. Based on forecasts for the Consumer Price Index from the S&P Global macroeconomic model, we assume inflation will average 6%–7% this winter compared with last winter. Given that rate of inflation, changes in expenditures and prices adjusted for inflation would be roughly 6%–7% less than the values reported.

Background. For this outlook, we define the winter heating season as October through March. Weather is a key input to our energy consumption forecast and based on the weather forecast from the National Oceanic and Atmospheric Administration (NOAA), we expect increases in winter energy consumption.

The average household winter energy expenditures discussed in this supplement are broad measures for comparing recent winters and reflect energy expenditures for all uses, not just heating. Fuel expenditures for individual households depend on the size and energy efficiency of individual homes and their heating equipment, along with thermostat settings and weather conditions. Each fuel also has its own market structure, physical infrastructure, regulations, and limitations that can affect the connection between wholesale and retail market events.

We use our Residential Energy Consumption Survey (RECS) as a baseline to estimate average energy consumption during the winter in each region. To develop our forecast household expenditures for natural gas, heating oil, electricity, and propane in this report, we group households by primary space heating fuel. We forecast total winter expenditures for all uses for each primary heating fuel, not just the portion attributable to heating. For example, the expenditures included for households that heat primarily with electricity in this report would also include electricity used for appliances and lighting. Because electricity has the widest range of uses among the fuels, electricity consumption tends to be less sensitive to changes in temperature than other fuels.

On average, we expect wholesale commodity natural gas prices to be higher this winter compared with last winter, which leads to higher prices for both natural gas and electricity in the retail market. Natural gas prices rose sharply earlier this year because consumption growth outpaced production growth in the first half of 2022. Strong demand growth resulted from growing liquefied natural gas (LNG) exports as well as a new market dynamic driving strong domestic natural gas demand: limited natural gas-to-coal switching in the electric power sector.

Wholesale price changes affect residential prices for natural gas and, particularly, electricity prices over relatively longer periods because these costs are incorporated into regulated rates. Even with this lag, increases in spot commodity prices over the past year are pushing up retail prices this winter. The Henry Hub natural gas spot price on September 30 was $6.40 per million British thermal units (MMBtu), which is 36% higher than last winter's average. These price increases contribute to our forecast that residential natural gas prices this winter will be 22% higher than last winter and that residential electricity prices will be 6% higher than last winter.

For the petroleum-based fuels, the price picture is mixed. Wholesale price changes for heating oil and propane are passed to consumers quickly. Crude oil prices increased sharply following Russia's full-scale invasion of Ukraine in February, but they have since declined, largely based on market concerns about the pace of economic and oil demand growth. On October 1, the benchmark Brent crude oil spot price was almost $90 per barrel (b), which was similar to the average from October through March of last winter. We expect crude oil prices this winter will average about $3/b higher than last winter. With crude oil prices relatively similar to last winter, retail prices for heating oil and propane are driven more by trends in the wholesale and retail markets for those fuels. We forecast average retail prices this winter for heating oil to be 16% higher than last winter and propane prices to be relatively close to last winter's average.

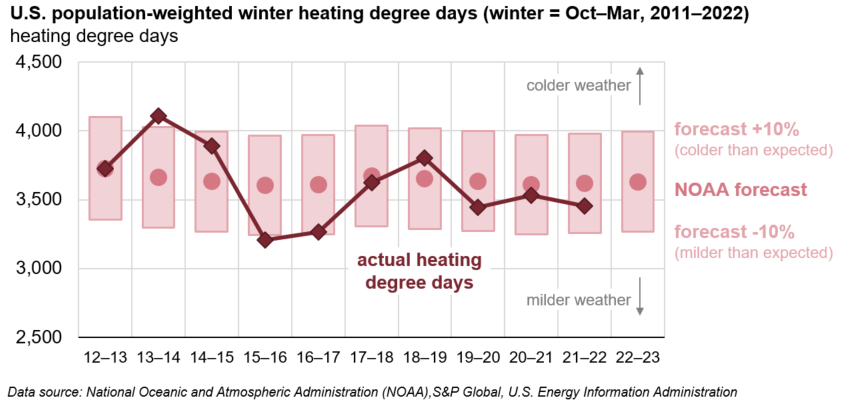

Based on NOAA's most recent winter forecast, we assume temperatures for the winter of 2022–23 in most of the country will be slightly colder than both last winter and the average winter for the previous 10 winters. We use heating degree days (HDDs) as a measure of how cold temperatures are compared with a base temperature—more HDDs indicate colder temperatures. On average, we expect 6% more population-weighted HDDs for the winter of 2022–23 across the United States than last winter and 2% more than the previous 10-winter average. Regionally, changes from last winter are fairly consistent. We forecast that the Northeast, Midwest, and West will all have 5% to 6% more HDDs this winter than winter 2021–22 and that HDDs in the South will be 9% more than last winter.

Because weather is a significant source of uncertainty in these forecasts, the Winter Fuels Outlook includes side cases where, measured in HDDs, all regions are 10% colder or 10% warmer than the baseline forecast. The prevailing high prices and low inventories for a number of fuels heading into this winter mean that even short spells of severe weather have the potential to affect energy markets.

Cold weather can affect household heating expenditures in two ways. First, cold weather raises the amount of energy required to keep a house at a specific temperature. Second, because cold weather raises demand and could cause supply disruptions, it can cause energy prices to rise, which could be more severe during a time of low fuel inventories. In the cases we consider, we adjust for both effects. We forecast that inventories will remain below the five-year average for heating oil and propane throughout this winter, driven by reductions in U.S. refining capacity and strong heating-related demand. We forecast that natural gas inventories will remain below the five-year average as electric power and heating demand remain strong, but natural gas inventories will narrow the deficit to the five-year average by the end of winter.

Natural Gas

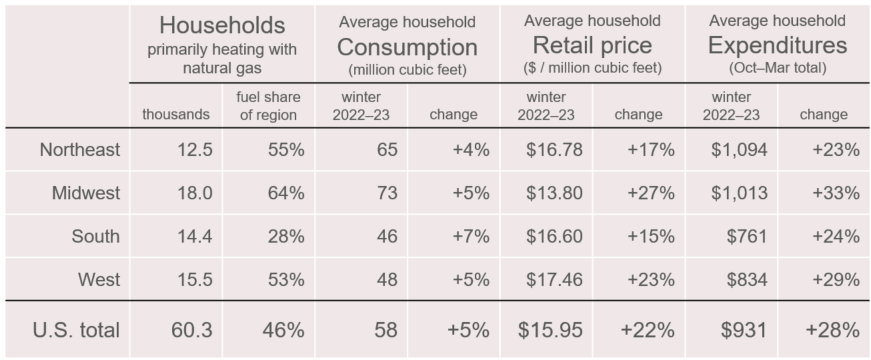

Nearly half of all U.S. households heat primarily with natural gas. We expect households that use natural gas as the primary space heating fuel will spend about $930 this winter, 28% more than they spent last winter. Our forecasted increase in natural gas expenditures is the result of both higher expected prices and consumption.

For households that use natural gas as their primary space heating fuel, we expect average household consumption for the winter to total 58 thousand cubic feet (Mcf), up 5% from last winter. We forecast a 4% to 5% increase in average natural gas consumption per household in the Northeast, Midwest, and West. We expect residential natural gas consumption in the South to be 46 Mcf this winter, up 7% from last winter.

The residential natural gas price for homes in the United States that heat primarily with natural gas will average about $16/Mcf, up from an average of $13/Mcf last winter. We forecast higher residential prices because of higher expected wholesale prices for natural gas in much of 2022 compared with 2021.

Changes in natural gas spot prices generally pass through to residential customers relatively slowly. Some state utility commissions set the rates that utilities can charge for natural gas deliveries a year or more in advance of billing to reflect the cost of wholesale natural gas that utilities purchased over many months. The timing and frequency of rate changes can vary by utility, however, and in times of high price volatility, some utilities make adjustments as often as several times in a year. In addition, residential prices include charges to cover utility operating costs and the cost to transport and distribute natural gas, which are not directly linked to wholesale commodity natural gas prices.

Although spikes in wholesale natural gas prices are not immediately reflected in retail prices, the additional cost of natural gas for utilities is typically passed on as smaller increases in retail prices over time. For example, regional natural gas spot prices reached record highs following Winter Storm Uri in February 2021, especially in the Midwest. Following that price spike, spot prices quickly returned to pre-winter-storm levels. Many utility companies in states affected by the storm filed motions with their states' public utility commissions detailing plans to recover costs that they had incurred as a result of the extremely high natural gas costs following the winter storm. These plans involve adding a line item charge to utility bills for the next several years to spread the cost out over a long period of time.

We forecast that residential natural gas prices will increase in all regions of the United States this winter, with natural gas spot prices at the U.S. benchmark Henry Hub averaging $7.26/MMBtu this winter, up 54% from last winter. We expect the largest increase in residential prices to occur in the Midwest, where we forecast that prices will average 27% higher than last winter. We expect residential natural gas prices to increase by 15% in the South, 17% in the Northeast and 23% in the West. If spot prices continue to rise, retail prices this winter could be even higher than our forecast.

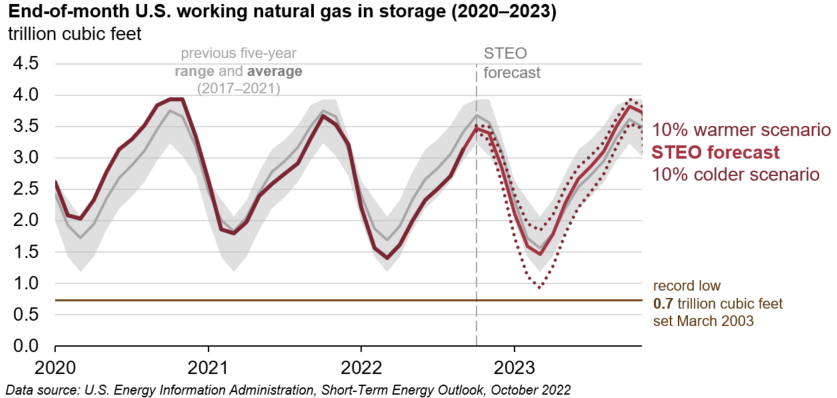

Natural gas inventories. Working natural gas inventories in our forecast reach almost 3.5 trillion cubic feet (Tcf) by the end of October, which would be 6% below the previous five-year average. U.S. natural gas storage injections usually take place from April through October, although injections often occur in early November, depending on temperatures and market conditions. Storage withdrawals typically occur from November through March. U.S. natural gas inventories began this injection season at the lowest level in three years because of high heating demand in January and record LNG exports. The above-average withdrawals last winter, combined with more-than-average consumption this summer, contribute to our forecast for below-average storage inventories heading into the winter heating season.

Although both spot and retail natural gas prices are higher in our forecast than last winter, under the baseline temperature case for this winter, we forecast draws in natural gas inventories will be less than the five-year average because we expect that increased demand this winter will be more than offset by growth in natural gas production. We expect U.S. dry natural gas production will be 2.8 Bcf/d (3%) higher than last winter. Our forecast for combined growth in consumption and exports this winter is 3.0 Bcf/d (3%). By the end of March 2023, we expect natural gas inventories to be 1.5 Tcf, which would be 7% less than the previous five-year (2018–2022) average.

As inventories narrow the deficit to the five-year average, we expect it will put downward pressure on natural gas prices later in the winter. In our forecast, monthly average Henry Hub spot prices peak near $7.70/MMBtu in January, before falling to around $6.50/MMBtu by March.

Warmer-than-forecast and colder-than-forecast side cases. In a 10% colder-than-forecast case, we expect natural gas inventories to end March 2023 at about 0.9 Tcf, which is 41% below the five-year average. In this case, Henry Hub spot prices would likely rise significantly above our forecast levels. In a 10% warmer-than-forecast case, inventories end March 2022 at 1.8 Tcf, which is 18% more than the five-year average.

Compared with the base case, forecast natural gas retail prices would be 5% higher in the colder-than-forecast case and consumption would be 13% higher, leading to expenditures that are 18% higher than in our base case. Because of the delay in the link between wholesale and residential natural gas prices, we expect increased consumption to have a larger effect on expenditures than price changes.

In a 10% warmer-than-forecast case, we forecast natural gas consumption would be 5% less than the base case, and prices would be 2% less, resulting in expenditures that would be 7% less than the base case.

We expect natural gas supplies to be adequate to meet winter demand; however, wholesale price volatility and localized wholesale price spikes could occur during severely cold temperatures. Wholesale price spikes resulting from constrained natural gas supplies can also have ripple effects through energy distribution systems. Higher wholesale prices or curtailments to electric power generators can cause electric generators to turn to other fuels during cold periods, which we have seen most typically in New England.

Heating Oil

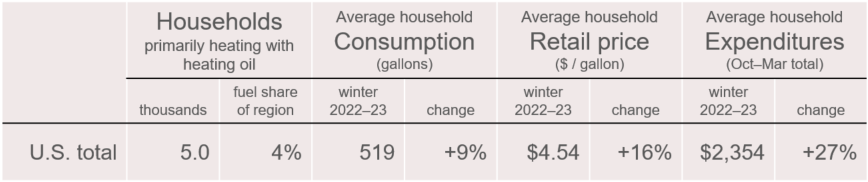

We expect that the 4% of U.S. households that use heating oil as the primary space heating fuel will spend about $2,350 on average this winter, up 27% from last winter. The increase in heating oil expenditures reflects our expectations for higher retail heating oil prices and more consumption than last year. We forecast that the average U.S. household will consume about 520 gallons of heating oil this winter, up 9% compared with last winter, which reflects NOAA's forecast of a colder winter. The retail price of heating oil in our forecast averages $4.54/gal during the winter of 2022–23, up 16% from the previous winter. Higher heating oil prices are driven by higher refining margins than last winter, partly offset by slightly lower crude oil prices.

Customers in the Northeast rely on heating oil more than in any other region. About 18% of households in this region use heating oil as a primary space heating fuel, down from 25% a decade ago. An increasing number of homes in the Northeast have switched to natural gas or electricity for primary space heating needs.

We expect retail heating oil prices to be 16% (64 cents per gallon [gal]) higher than last winter. Higher refinery margins for heating oil (which we calculate as the price difference between wholesale heating oil and Brent crude oil) drive this increase. For winter 2022–23, we forecast that wholesale heating oil margins will average $1.06/gal, which would be 60 cents/gal higher than last winter and 71 cents/gal higher than the previous five-winter average. Our forecast for heating oil margins this winter reflects price pressures that have currently been affecting the U.S. distillate market, including low inventories, low imports, and limited refining capacity.

In our forecast, the Brent crude oil price, which is the most relevant crude oil price in determining U.S. petroleum product prices, averages $2.22/gal, or $93/barrel (b) this winter, which would be 7 cents/gal higher than last winter. The Brent crude oil price averaged $79/b in 4Q21 but increased to $101/b in the 1Q22, resulting in an average Brent crude oil price of $90/b for last winter. The increase in 1Q22 partly resulted from geopolitical risk associated with Russia's full-scale invasion of Ukraine, as well as increasing demand that outpaced increases in crude oil production. Global crude oil prices continued to increase in 2Q22, but they fell in 3Q22 as a result of rising global oil inventories, a stronger U.S. dollar, and slowing oil demand growth. However, we expect crude oil price pressures to be more to the upside in the coming month following the OPEC+ announcement of a production cut on October 5, which are reflected in this outlook. Our previous forecast had already included a reduction in OPEC+ crude oil production that was largely consistent with the announced cuts, but the announcement increases the potential for global oil production to be lower than our forecast.

Any deviation in crude oil prices or margins from our forecast would cause a similar deviation in retail heating oil prices and consumer expenditures. Changes in prices of crude oil and wholesale heating oil pass through to the retail heating oil price much more quickly than changes in the wholesale price of other heating fuels, such as natural gas and electricity, pass through to retail prices for those fuels. In addition, many heating oil users buy supplies ahead of the winter and refill as needed. When forecasting expenditures, our analysis does not account for heating oil that consumers purchased ahead of time.

Relatively low global natural gas and coal supplies can affect U.S. distillate markets because certain international markets use distillate fuel for power generation if prices of natural gas or coal become uneconomical or if supplies of those fuels are unavailable. Lower natural gas moving from Russia into Europe may further contribute to lower international distillate availability. With the impending implementation of the European Union's ban on Russia's petroleum products in February 2023, the potential for increased fuel switching from natural gas to distillate presents a greater source of price uncertainty than in previous years.

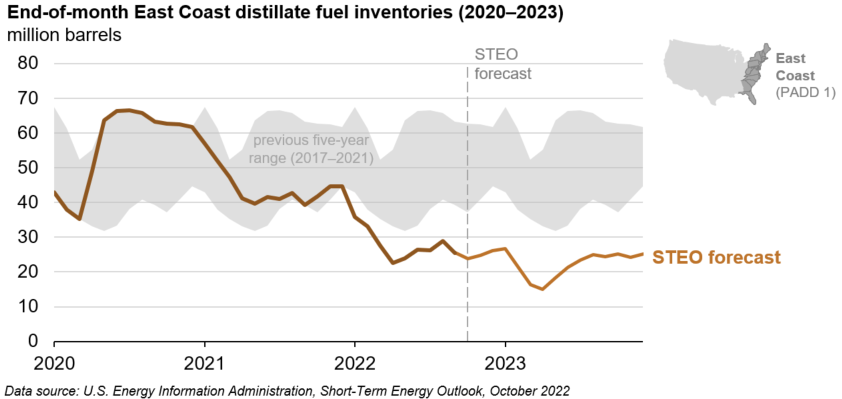

Distillate fuel inventories. Distillate fuel inventories (which include heating oil and diesel fuel) on the East Coast (PADD 1) at the end of September were 25.5 million barrels, 45% below the five-year average.

Almost 60% of East Coast distillate inventories are in the Northeast (PADD 1A and PADD 1B). Inventories in the Northeast ended September 57% below the five-year average. Several factors have contributed to low distillate inventories in this region, including:

- Limited regional refining capacity

- Increasing domestic distillate demand in the first half of the year

- Low imports as a result of generally tight distillate markets worldwide

Although refineries on the East Coast are running at close to their capacity, regional refining capacity has fallen in recent year. In 2019, the Philadelphia Energy Solutions refinery, the region's largest, was shut down permanently following a fire. From January through September 2022, East Coast (PADD 1) refinery utilization averaged 91%, and gross refinery inputs averaged 15% less than the five-year average.

In the context of reduced imports and limited refining capacity, relatively strong distillate demand early in the year contributed to low inventories. In the first half of 2022 (1H22), East Coast product supplied of distillate fuel oil (a proxy for consumption) was slightly higher than in 2021, nearly equal to the five-year average. Weekly data, however, indicate that in recent weeks national distillate consumption has fallen (data for regional consumption is not available on a weekly basis).

The current low inventories relative to previous years are likely to put upward pressure on heating oil prices throughout the winter. Although a number of supply options are available in the Northeast (including pipeline shipments from other U.S. regions, imports from international markets, and coastwise compliant shipments from other U.S. ports), low international inventories suggest that the potential for imports from international markets may be less than in previous years. Periods of severe cold weather could also lead to more withdrawals from inventories and higher distillate prices, which could put additional pressure on already low distillate inventories.

Although refining margins are well above their previous five-year high, the ability to increase refinery utilization or yields in response to winter distillate demand is limited. We forecast gross refinery inputs will average 15.8 million barrels per day (b/d) this winter, which is 2% lower than last winter. This winter, we expect refinery and blender production of distillate fuel will average 4.8 million b/d (almost identical to last winter).

Distillate fuel imports and exports. Imports of distillate fuel into the East Coast in 1H22 averaged 167,000 b/d, down 40% from 1H21. Prior to Russia's full-scale invasion of Ukraine in February, Russia was a leading supplier of distillate fuel to Europe. U.S. and UK sanctions on Russia from the invasion and the independent choices of private sector companies to abstain from trade with Russia have reduced distillate supplies coming from Russia. In addition, demand for distillate fuel in Europe's electric power sector has increased because of record-high natural gas prices in Europe, further tightening Atlantic Basin distillate markets. This year, U.S. East Coast imports of distillate fuel averaged 361,000 b/d in February and fell to an average of 113,000 b/d from March through June.

Warmer-than-average and colder-than-average side cases. Based on the NOAA outlook, our forecast assumes the Northeast, where home heating with heating oil is most prevalent, will be 5% colder than last winter. If the winter is 10% colder than forecast, we expect that average household expenditures for heating oil would be 11% higher than the base case. With colder-than-expected temperatures, we forecast 1% higher heating oil prices and 9% more heating oil consumption relative to the base case.

Because U.S. heating oil is a relatively small part of the global distillate market, cold weather tends to have less of an effect on distillate and crude oil market conditions than for fuels such as propane and natural gas. Cold weather can affect local retail heating oil markets if supply conditions become constrained, which could put upward pressure on retail margins. Because of high natural gas prices worldwide, cold weather could affect retail heating oil prices more than in recent years if distillate fuel is substituted for natural gas in power generation, leading to upward pressure on distillate refining margins.

In the 10% warmer scenario, we forecast expenditures will be 9% less than the base case, resulting primarily from consumption that is 9% less than the base case and prices that are slightly lower.

Electricity

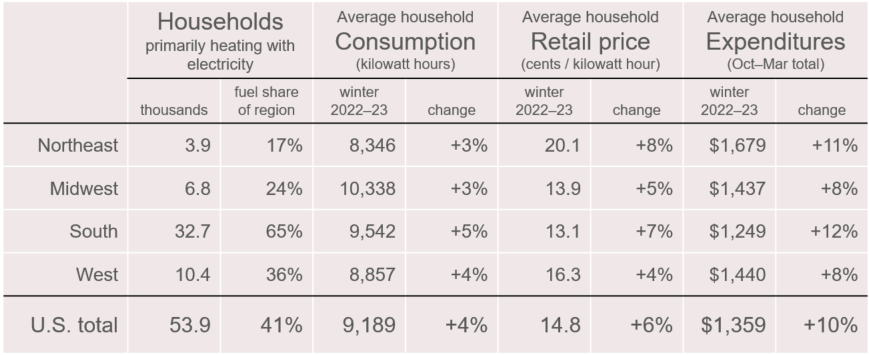

We forecast that U.S. households that heat primarily with electricity will spend 10% more on electricity than last winter, at an average of about $1,360. This increase is based on our forecast of 4% more electricity consumption and 6% higher residential electricity prices. Nearly all U.S. households use electricity in some form, but 4 out of 10 households rely on electric heat pumps or electric resistance heaters as the primary source for space heating. Nearly two-thirds of homes in the South heat primarily with electricity. Electric heaters are also commonly used as a secondary heating source in many U.S. homes.

We forecast that winter expenditures for electricity customers in the Northeast will grow by 11% from last winter, reflecting 8% higher prices and 3% more consumption. In the South, we forecast 12% higher winter electricity expenditures because of higher forecast prices and expected colder winter weather. In the Midwest and West, we forecast winter expenditures will average 8% more than last year.

We expect U.S. electricity prices for residential customers will be 6% higher this winter than last winter, at an average 14.8 cents per kilowatthour. Prices during the winter of 2021–2022 grew by a similar percentage, but year-over-year growth in nominal winter electricity prices had averaged only about 1% each year between 2015 and 2021.

Electricity prices charged to ultimate customers reflect the costs of supplying the electricity and delivering it to households. During the first seven months of this year, the cost of natural gas purchased by U.S. electric generators averaged $6.61/MMBtu, which is 33% more than the average cost during the same period last year and almost three times the cost in 2020. Higher fuel costs have led to higher wholesale power prices nationwide. Wholesale prices are highest in the Northeast, with prices in the ISO New England market averaging $96 per megawatthour during the first nine months of 2022, which is double the average price in 2021.

Changes in electricity supply costs can take time to translate to changes in retail rates. Increases in costs pass through to customers more quickly in areas of the country with deregulated markets where consumers have a choice of electricity providers. We expect residential electricity price increases this winter will range from 8% in the Northeast, where many states have deregulated retail electricity distribution, to 4% in the West.

Our forecast of winter residential electricity consumption reflects total electricity use, including lighting, appliances, and electronics. In homes that primarily heat with electricity, overall winter temperatures can significantly affect the amount of electricity consumed by residential households. We expect colder weather, with more heating degree days this winter compared with last year, and with the largest increase (9%) occurring in the South, where most households heat with electricity. As a result, we expect 4% more U.S. residential electricity consumption this winter than last winter.

Warmer-than-forecast and colder-than-forecast side cases. In the side case that assumes a 10% colder-than-forecast winter, we forecast expenditures for electricity will be 9% higher this winter than the base case. In this case, electricity prices will be similar to the base case and consumption will be 10% higher than the base case.

In the case that assumes a 10% warmer-than-forecast winter, we forecast expenditures for electricity will be 2% less than the base case. In this case, consumption will be 2% less than the base case and prices will be relatively similar.

Electricity generation shares by fuel type. The fastest-growing source for generating electricity in the United States is renewables, especially wind and solar. By December 2022, we expect the U.S. electric power sector will have 26% more solar generating capacity than last December (increasing from 61 to 77 gigawatts) and 9% more wind power capacity (totaling 144 gigawatts). We forecast that wind and solar combined will contribute 16% of U.S. total generation in winter of 2022-23, up from nearly 15% last winter.

Natural gas still provides the largest share of U.S. electricity, which we forecast will contribute 36% of total generation during winter 2022–23, unchanged from last winter. We expect natural gas generation to remain near record levels this winter despite the higher natural gas prices, because coal-fired power plants, which have traditionally acted as alternatives to natural gas, are facing fuel supply constraints. The coal generation share in the forecast averages 20% this winter, down from 21% in winter 2021–22.

Propane

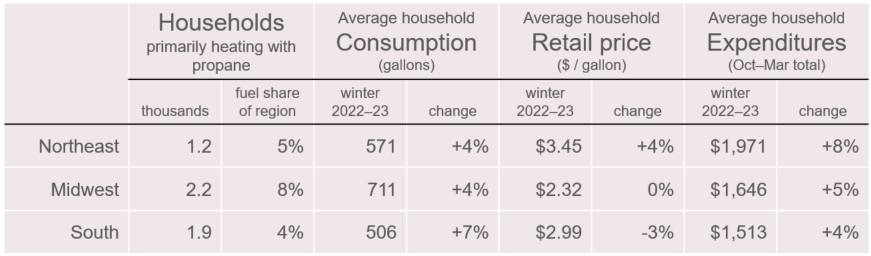

About 5% of all U.S. households use propane as the primary space heating fuel. We forecast that households in the Northeast, Midwest, and South will spend 5% ($80) more, on average, for propane this winter compared with last winter, driven by higher expected consumption. We do not forecast expenditures for the West Coast because we do not collect propane price data for the West Coast in our surveys.

We expect that households heating with propane in the Northeast will spend an average of $1,970 per household, which is 8% more than last winter. Our forecast increase in Northeast expenditures for propane-fueled heating is based on our forecast that the region's propane prices will be 4% higher and there will be 4% more household propane consumption, on average. We expect households in the Midwest to spend 5% more than last winter (an average of $1,650 per household), reflecting a forecast 4% increase in propane consumption from last winter and slightly higher propane prices. In the South, we expect households to spend 4% more than last winter (an average of about $1,510 per household), reflecting an average 7% increase in consumption offset by a 3% decrease in propane prices.

Similar to heating oil, changes in wholesale propane prices pass through relatively quickly to retail propane prices, and many propane users buy supplies ahead of the winter and refill as needed. When forecasting expenditures, our calculations do not account for propane that consumers purchase ahead of its use or propane that was contracted at prices set before the start of the winter. We assume consumers use the propane at the time they purchase it, at the prevailing retail price.

As of September 30, the propane spot price at the Mont Belvieu Hub, near Houston, had dropped to 87 cents/gal, which is 40% less than the same time in 2021. Last winter, high winter heating consumption and increased global demand for propane contributed to low U.S. propane inventories and high propane prices. Throughout last winter the wholesale propane price had been higher relative to the benchmark crude oil price than is typical. In March 2022, the propane spot price reached its highest inflation-adjusted price since February 2014. Since March 2022, the wholesale propane price has steadily decreased to less than $1.00/gal. This year, the propane-crude oil price relationship has returned to historically typical levels, partly reflecting higher propane inventories to start the winter, albeit inventories that are below the five-year average.

We expect U.S. propane consumption across all sectors to be up about 2% this winter compared with last winter, which results from an increase in propane use for space heating and for petrochemical production that is partly offset by lower propane use as a fuel for drying agricultural crops early in the winter heating season. For this outlook, we assume agricultural consumption for drying grain will fall below last year's level. Low precipitation and the poor condition of this year's corn crop is allowing crops to dry in the fields, requiring less drying in propane-fueled commercial grain dryers.

Propane inventories. Propane inventories typically build in the United States between April and October and begin drawing down in late September or October, when agricultural use of propane rises and heating use picks up. We estimate that at the end of September, U.S. propane (including propylene) inventories were more than 84 million barrels, about the same as the five-year average but 15% more than at the same time last year. At the end of September, inventories in the U.S. Gulf Coast (which account for about 55% of all U.S. inventories) were 4% more than the five-year average, and in the Midwest (which accounts for almost 30% of U.S. inventories) they were 9% below the five-year average. Inventory levels in the Northeast were 2% above their five-year averages.

Propane inventory builds in the United States, and particularly on the Gulf Coast, were limited this summer as a result of global propane market dynamics. U.S. propane exports averaged almost 1.4 million b/d during the first seven months of 2022, the most on record during that period. Global demand of U.S. propane was strong because of rising consumption in the petrochemical sector.

We forecast that propane inventories will remain below their previous five-year average, but inventory deficits to the five-year average will likely not widen significantly further during the heating season. In the colder-than-forecast side case, propane inventories would fall to 19 million barrels at the end of March, which would be the least on record in data going back to 1973.

Propane imports and exports. We forecast U.S. propane exports this winter will be greater compared with last winter as a result of strong global demand for propane as a petrochemical feedstock as well as more exports to Europe for winter heating. Propane inventory levels in Western Canada, which are near the five-year average, are increasingly being used for export at their two marine terminals, which may limit the quantity of propane available for import into the Midwest.

Warmer-than-forecast and colder-than-forecast side cases. Weather will be a key determinant of propane market outcomes and consumer expenditures this winter. If the winter is 10% colder, we expect significant upward pressure on wholesale propane prices that would quickly be passed along to retail prices and affect consumer expenditures.

In the 10% colder side case, we forecast that household expenditures for propane will be 26% higher than the base case in the Northeast, 35% higher in the Midwest, and 25% higher in the South. In the 10% warmer scenario, our forecast expenditures are about 16% lower across all three regions compared with the base case.

Wood

We estimate that more than 1.7 million U.S. households, or 1.3%, will use cord wood or wood pellets as the primary fuel for residential space heating this winter.

As of 2020, we estimate another 7% of households will use wood as a secondary source of heat, second to electricity as a supplemental heating fuel for U.S. households. Wood is more widely used in rural homes, with 22% of rural U.S. households using wood for primary or secondary space heating, compared with 6% of urban households, according to RECS. Wood use was most common in New England, where 16% of households used wood as either a primary or secondary source of heat.

yeagerationestreen.blogspot.com

Source: https://www.eia.gov/outlooks/steo/report/winterfuels.php

0 Response to "Will Gas and Oil Price Continue to Decline September 2017"

Postar um comentário